Loan Calculator

Results:

Monthly Payment: -

Total Interest: -

Total Payment: -

Introduction

Loan Calculator is one of the most important calculator. In today’s financial landscape, loans are an essential part of many people’s lives. Whether you are purchasing a house, financing a car, or funding a business, loans provide the necessary capital to achieve your goals. However, understanding the financial commitment of a loan is crucial to making informed decisions. This is where a loan calculator comes in handy. A loan calculator helps you estimate monthly payments, total interest, and overall costs, ensuring you can plan your finances effectively. In this article, we will explore the importance of loan calculators, how they work, and why you should use one before borrowing money.

Table of Contents

What is a Loan Calculator?

A loan calculator is a financial tool designed to help users estimate their monthly loan repayments. It considers key factors such as the loan amount, interest rate, and loan term to determine how much you will pay each month and over the entire loan period. By using a loan calculator, you can make an informed decision about whether a loan is affordable for you and how different variables impact the repayment process.

How Does a it Work?

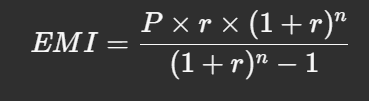

A loan calculator typically uses the Equated Monthly Installment (EMI) formula:

Where:

- P = Loan amount (Principal)

- r = Monthly interest rate (Annual interest rate / 12 / 100)

- n = Number of months for loan repayment

This formula calculates how much you need to pay each month, ensuring that you can plan your finances accordingly.

Example Calculation

Let’s say you take a $20,000 loan with an annual interest rate of 6%, to be repaid over 5 years.

- Loan amount (P): $20,000

- Interest rate (r): 6% annually (0.06 / 12 = 0.005 per month)

- Loan term (n): 5 years (60 months)

Using the formula, your monthly EMI would be approximately $386.66. Over the loan term, the total repayment would be around $23,199.60, which includes $3,199.60 in interest.

Benefits

1. Financial Planning

A loan calculator helps you plan your finances by giving a clear picture of your monthly obligations. This prevents situations where you might take a loan that is beyond your repayment capacity.

2. Quick and Easy Comparison

Instead of manually calculating loan costs, a loan calculator instantly provides results, making it easier to compare different loan offers from banks and lenders.

3. Better Decision Making

By knowing how much interest you’ll pay over time, you can decide whether to go for a shorter loan term with higher EMIs or a longer term with smaller monthly payments.

4. Avoiding Over-Borrowing

It helps you determine how much you can afford to borrow without putting a strain on your finances. This prevents situations where excessive debt leads to financial instability.

Types of Loans You Can Calculate

It can be used for different types of loans, including:

- Personal Loans – Unsecured loans for personal use.

- Home Loans – Long-term loans for purchasing property.

- Auto Loans – Loans specifically for vehicle purchases.

- Student Loans – Education loans for tuition and related expenses.

- Business Loans – Loans to fund business operations or expansion.

Each loan type may have varying interest rates and terms, which can be easily analyzed using a loan calculator.

How to Use a Loan Calculator Effectively

To use calculator, follow these steps:

- Enter the Loan Amount – Input the amount you wish to borrow.

- Select the Interest Rate – Use the rate offered by your lender.

- Choose the Loan Term – Specify the repayment duration.

- Analyze the Results – Check the EMI, total interest, and overall repayment amount.

- Adjust Variables – Experiment with different loan amounts and terms to find the best option for you.

Quora

Frequently Asked Questions (FAQs)

1. Is a loan calculator accurate?

Yes, loan calculators provide a highly accurate estimate of your loan payments. However, the actual amount may vary slightly due to lender-specific fees and policies.

2. Can I use a loan calculator for mortgage loans?

Absolutely! A mortgage loan calculator follows the same principles and helps determine your monthly home loan payments.

3. What happens if I make extra payments?

Extra payments reduce the principal amount, leading to lower interest costs and a shorter loan term. Some advanced loan calculators allow you to factor in extra payments.

4. Do all lenders use the same EMI formula?

Most lenders use the standard EMI formula, but some may have different interest calculation methods (such as reducing balance interest). Always confirm with your lender.

5. Is it better to take a shorter loan term?

A shorter loan term means higher monthly payments but lower overall interest costs. A longer term results in smaller EMIs but higher total interest paid.

Conclusion

A loan calculator is a powerful tool that simplifies the loan decision-making process. Whether you’re planning to take a personal loan, mortgage, or business loan, using a calculator ensures that you borrow wisely and within your means. By understanding your repayment obligations beforehand, you can avoid financial pitfalls and make informed borrowing choices.

Before applying for any loan, make sure to use a loan calculator to compare different options and find the best deal. It only takes a few seconds but can save you thousands of dollars in the long run!

About Us

1 thought on “Loan Calculator – Estimate Your Loan Instantly – 2025”