Mortgage Calculator

A mortgage calculator is a powerful tool that helps homebuyers and homeowners estimate their monthly mortgage payments. It provides insights into loan affordability, interest costs, and repayment schedules. Whether you are purchasing a new home or refinancing an existing mortgage, a mortgage calculator allows you to make informed financial decisions.

What is a Mortgage Calculator?

A mortgage calculator is an online tool that calculates the estimated monthly payment for a home loan. By entering the loan amount, interest rate, and loan term, users can determine how much they will need to pay each month. This tool simplifies complex calculations and provides instant results, making it easier to plan a budget.

Table of Contents

How Does a Mortgage Calculator Work?

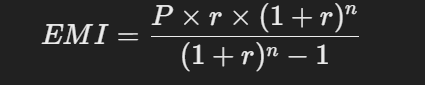

A mortgage calculator uses the following formula to compute monthly payments:

Where:

- EMI = Monthly mortgage payment

- P = Loan amount (principal)

- r = Monthly interest rate (annual interest rate / 12)

- n = Number of months in the loan term

For example, if you take out a $300,000 loan at a 4.5% annual interest rate for 30 years, your estimated monthly mortgage payment will be $1,520.06.

Key Components of a Mortgage Loan

1. Loan Amount

The loan amount, or principal, is the total sum borrowed from a lender to purchase a home. Larger loan amounts lead to higher monthly payments and more interest paid over time.

2. Interest Rate

The interest rate is the percentage charged by the lender for borrowing money. Lower interest rates result in lower monthly payments and less interest over the life of the loan. Mortgage rates are influenced by credit scores, economic conditions, and loan types.

3. Loan Term

The loan term is the duration for repaying the loan. Common terms are 15, 20, or 30 years. Shorter loan terms lead to higher monthly payments but lower overall interest costs. Longer loan terms reduce monthly payments but increase total interest paid.

4. Down Payment

A down payment is an upfront amount paid toward the home’s purchase price. A higher down payment reduces the loan amount, resulting in lower monthly payments and interest costs.

5. Property Taxes and Insurance

Lenders often include property taxes and homeowners insurance in mortgage payments. These costs vary based on location and property value.

Benefits of Using a Mortgage Calculator

1. Helps You Plan Your Budget

A mortgage calculator allows you to estimate monthly payments and determine whether a loan fits within your financial limits. This helps in setting a realistic home-buying budget.

2. Allows Loan Comparison

By adjusting the loan amount, interest rate, and term, you can compare different mortgage options and choose the most affordable one.

3. Saves Time and Effort

Instead of manually calculating mortgage payments, the calculator provides instant results, saving time and reducing the risk of errors.

4. Shows Interest Costs Over Time

The calculator breaks down the total interest paid over the loan’s lifetime, helping you understand the long-term cost of borrowing.

5. Helps in Decision-Making

Whether you are buying a new home or refinancing, a mortgage calculator enables you to make well-informed financial decisions.

Factors That Affect Your Mortgage Payments

1. Credit Score

A higher credit score leads to lower interest rates, reducing monthly payments and overall loan costs. Lenders prefer borrowers with strong credit histories.

2. Loan Type

There are different types of mortgage loans, including:

- Fixed-Rate Mortgages: The interest rate remains the same for the loan term.

- Adjustable-Rate Mortgages (ARM): Interest rates fluctuate based on market conditions.

- FHA Loans: Government-backed loans with lower down payment requirements.

- VA Loans: Loans available to veterans and active military members.

3. Economic Conditions

Mortgage rates change based on inflation, Federal Reserve policies, and market trends. Monitoring these factors can help you secure the best loan terms.

How to Lower Your Mortgage Payments

- Improve Your Credit Score – Pay bills on time and reduce outstanding debt.

- Choose a Longer Loan Term – A 30-year loan has lower monthly payments than a 15-year loan.

- Make a Higher Down Payment – Paying more upfront reduces the principal amount.

- Refinance to a Lower Interest Rate – Refinancing can lower your monthly mortgage payments if interest rates drop.

- Consider Extra Payments – Making additional payments can reduce loan tenure and total interest paid.

Quora

Mortgage Calculator Example

Scenario 1: Standard Home Loan

- Loan Amount: $250,000

- Interest Rate: 5%

- Loan Term: 30 years

Estimated Monthly Payment: $1,342.05

Total Interest Paid Over 30 Years: $233,139

Scenario 2: Refinancing with a Lower Interest Rate

- Loan Amount: $250,000

- Interest Rate: 3.5%

- Loan Term: 30 years

Estimated Monthly Payment: $1,122.61

Total Interest Paid Over 30 Years: $154,139

By reducing the interest rate from 5% to 3.5%, the monthly payment drops by $219.44, and total interest savings over 30 years is $79,000.

Conclusion

A mortgage calculator is a valuable tool for anyone looking to buy a home or refinance an existing loan. It provides a clear estimate of monthly payments, helping borrowers plan their finances effectively. By understanding key mortgage components like interest rates, loan terms, and down payments, you can make informed decisions that align with your financial goals.

If you’re planning to take out a mortgage, using a mortgage calculator can save you time, help you compare loan options, and give you a better understanding of your overall borrowing costs. Always consider factors like credit scores, market conditions, and additional costs when choosing the best mortgage for your needs.

Other Calculators:

Loan Calculators

Interest Calculator

1 thought on “Mortgage Calculator – Plan Your Home Loan Payments – 2025”